News

05 - 06 - 2026

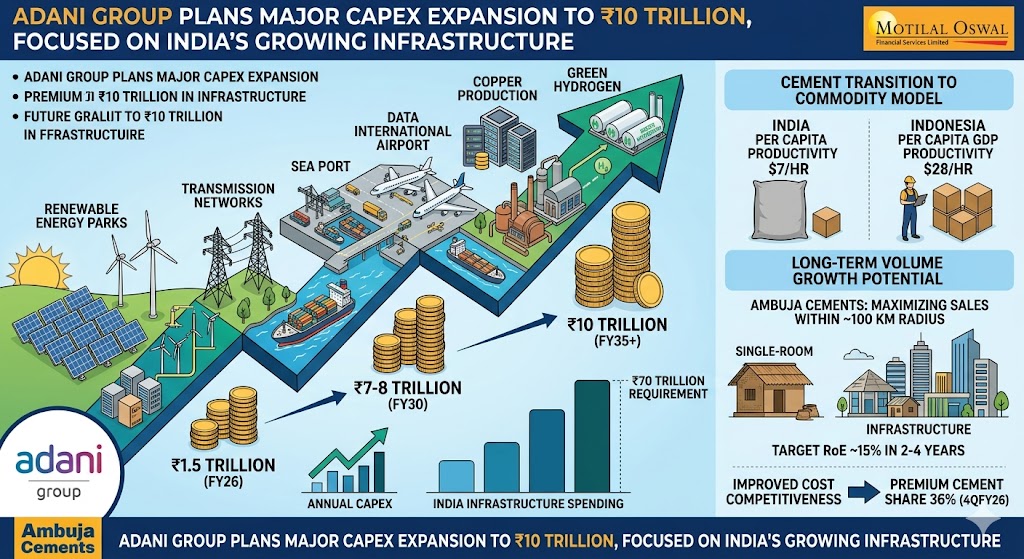

Adani Group to hike capex to ₹7-8 lakh crore by FY30

The group had invested ₹1.5 trillion in FY26, the largest by an Indian corporate.

India’s Adani Group plans to increase capital expenditure (capex) to ₹7-8 trillion by financial year 2030 (FY30) and further to ₹10 trillion, banking on the growing infrastructure in the country.

The investment pipeline spans across renewable energy parks, transmission networks, seaports, airports, data centres, copper, and green hydrogen projects, according to a Motilal Oswal Financial Services Limited (MOSFL) report.

MOSFL said it attended a group meeting with Adani Group CFO.

The group had invested ₹1.5 trillion in financial year 2026 (FY26), which according to an earlier report by brokerage Angel One marked the largest annual investment programme by an Indian corporate.

According to MOSFL, the current annual infrastructure spending levels in India are about ₹17 trillion against an estimated requirement of ₹70 trillion. Adani Group indicated that India’s per capita gross domestic product (GDP) productivity is at $7 per hour, much below Indonesia’s $28 per hour.

Quoting Adani management, MOSFL said that the investments will remain disciplined, with each business pursuing projects that generate returns above the cost of capital. Capital allocation decisions are made independently by each operating company.

Cement to transition to commodity model

In the cement sector, management expects the Indian market to change over time, with cement eventually being sold as a commodity rather than a branded product. The group anticipates long-term volume growth potential driven by low cement penetration in housing, infrastructure, roads and logistics. Nearly half of Indian households live in single-room dwellings, many of which are partially cemented or constructed using traditional materials.

Returns on investments (RoI) in the cement business remain lower than expected. The group has targeted a return on equity (RoE) of about 15 per cent to be achieved over the next 2-4 years as capacity additions are absorbed. To improve cost competitiveness, companies are maximising sales within a radius of about 100 km from manufacturing facilities.

Ambuja Cements’ premium cement share stood at about 36 per cent of trade sales in the fourth quarter of financial year 2026 (4QFY26), compared with 29 per cent recorded during the same quarter of last fiscal. Lead distances remain elevated due to the concentration of limestone mines, which companies are mitigating through split-location grinding units, optimising scale operations, and increasing direct dispatches.

MOSFL maintained a buy rating on Ambuja Cements with a target price of ₹530.

The brokerage estimates a compound annual growth rate of 11 per cent in consolidated revenue, 18 per cent in EBITDA, and 19 per cent in net profit through FY26-28 for Ambuja Cements, led by volume growth of 9 per cent and a 2 per cent improvement in realisation.

Ambuja Cement’s EBITDA per tonne is estimated to be at ₹856 in FY27 and ₹1,053 in FY28, against ₹887 in FY26. The company is estimated to shift from a net cash position of ₹910 crore in FY26 to a net debt of ₹790 crore in FY27 and ₹2,290 crore in FY28.

Most Popular

3 days ago

Indian’s Education Minister Dharmendra Pradhan resigns

In an X post, Pradhan said the resignation was to prevent anti-national forces from…

3 days ago

Pralhad Joshi given additional charge of Education Ministry

This follows the resignation of Dharmendra Pradhan amidst intense, weeks-long protests over alleged exam…

1 day ago

After Aadhaar, Nilekani to solve India’s exam trust crisis

The Indian government’s decision to appoint Nilekani to head a high-powered task force on…

1 day ago

Power systems performance remains strong for CG Power

Key risks for the company include a slowdown in T&D capex, an increase in…