Analysis

08 - 06 - 2026

Fitch expects Brent oil average at $87/bbl on late July Hormuz reopening

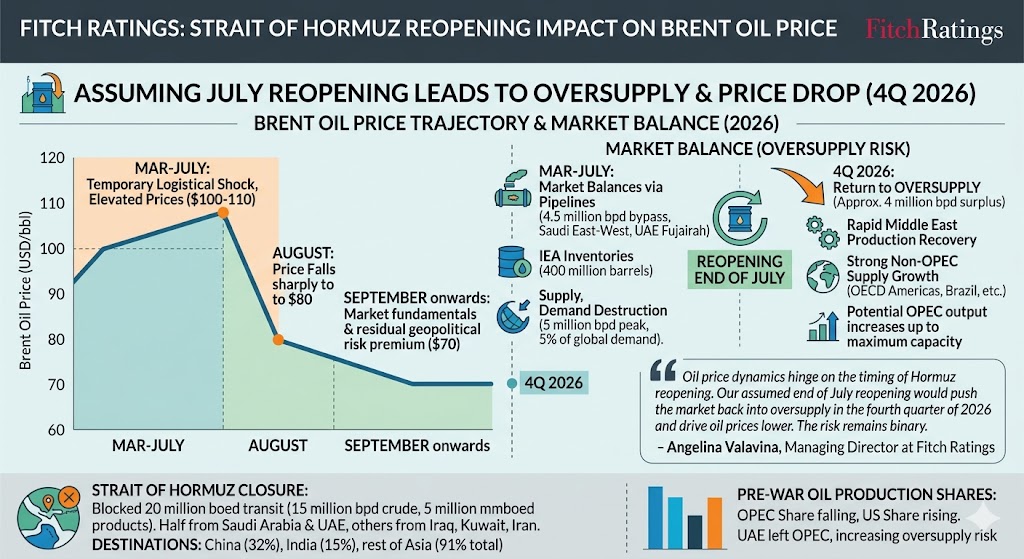

Assuming the strait reopens by July-end, the Brent is expected to fall sharply from the elevated March-July levels. The market would return to oversupply levels from September 2026

Fitch Ratings expects Brent oil price to hover about $87 a barrel (bbl), assuming the Strait of Hormuz reopens by the end of July, which would also lead to an oversupply.

The current escalation in oil prices reflects a temporary logistical supply shock rather than a lasting loss of production capacity, the rating agency said in a note.

Assuming the strait reopens around the end of July, the Brent is expected to fall sharply from the elevated March-July levels. The market would return to oversupply levels from September 2026 due to a lack of material damage to regional oil infrastructure, rapid recovery in Middle East production, and strong non-Organization of the Petroleum Exporting Countries (OPEC) supply growth.

Further, a potential OPEC output increases up to a maximum production capacity will also help.

Consequently, Brent is assumed to average $100-110 a barrel in May to July, before falling to $80 a barrel in August and to about $70 a barrel from September. The latter level is implied by market fundamentals plus a residual geopolitical risk premium.

“Oil price dynamics hinge on the timing of Hormuz reopening. Our assumed end of July reopening would push the market back into oversupply in the fourth quarter of 2026 and drive oil prices lower. The risk remains binary,” Angelina Valavina, managing director at Fitch Ratings, said.

SUPPLY CHANNELS, INVENTORIES

The effective closure of the Strait of Hormuz by Iran blocked the transit of 20 million barrels of oil equivalent per day (mmboed), which includes 15 million barrels per day (bpd) of crude oil and 5 million mmboed of oil products. This volume accounts for 20 per cent of global oil consumption, it added.

Saudi Arabia and the UAE accounted for half of the oil volumes transported through the strait before the conflict, while the remainder comprised exports from Iraq, Kuwait, and Iran. China and India were the destinations for half of these exported volumes.

The global oil market is expected to balance during the five-month closure through July via alternative pipelines, the release of 400 million barrels of inventories by the International Energy Agency (IEA), additional supply, and demand destruction.

Saudi Arabia’s East-West pipeline provides export capacity, while the UAE operates a pipeline to the Fujairah export terminal. Together, these pipelines provide 4.5 million bpd of spare capacity to bypass Hormuz, compared with the 15 million bpd of crude oil volumes that previously transited the strait.

There was a material demand destruction of 5 million bpd during the closure period, representing about 5 per cent of global oil demand. In March, demand destruction stood at 0.8 million bpd, averaging 1.6 million bpd across March and April.

REGIONAL VOLUMES, SURPLUS RISK

Asia accounted for 91 per cent of the oil sold through the strait before the conflict, with 32 per cent going to China and 15 per cent to India. China’s oil stocks stood at 1.2 billion barrels out of a global total of 8.2 billion barrels in January 2026.

Production in Organisation for Economic Co-operation and Development (OECD) Americas, Kazakhstan, Venezuela, Brazil, and Russia increased by 1.4 million bpd between February and April 2026. Fitch forecasts global oil supply to be about 2.9 million bpd lower on average in 2026 than in 2025, but expects the market to revert to a surplus of about 4 million bpd in the fourth quarter of 2026.

OPEC’s share of global oil production fell to 34 per cent in 2024 from 47 per cent in 1970, while the US share rose to 21 per cent in 2024 from 10 per cent in 2000. The UAE’s recent decision to leave OPEC, where it produced 3.6 million bpd or 12 per cent of OPEC’s output before the war, signals a shift to a volume over value strategy, implying weaker discipline and a higher risk of oversupply.

Most Popular

1 day ago

Power systems performance remains strong for CG Power

Key risks for the company include a slowdown in T&D capex, an increase in…

3 days ago

Indian’s Education Minister Dharmendra Pradhan resigns

In an X post, Pradhan said the resignation was to prevent anti-national forces from…

1 day ago

Infosys fined in France over employee work-hour tracking failures

The action reflects the strict oversight of workplace practices in France, where companies are…

23 hours ago

India’s private space tech firms raise $871 million, Skyroot becomes first unicorn

Skyroot became India's first SpaceTech unicorn following a $50 million Series C round in…