Analysis

05 - 06 - 2026

Execution takes centre stage as Indian fashion retail exits discount era

The broader takeaway into FY27 is that Indian fashion retail is no longer competing only on growth, ccording to a report by Yes Securities.

The Indian fashion retail sector is now moving into a far more execution-sensitive phase, moving away from the heavy discounting, inventory clean-up and demand volatility that bogged it down over the last few years.

The demand for the sector improved meaningfully from mid-February onwards aided by weddings, summer demand and better footfalls. However, management commentary across players increasingly focused on margin quality, sourcing pressures and productivity rather than outright demand recovery, according to a report by brokerage firm Yes Securities.

Rising raw material costs linked to geopolitical disruptions and polyester inflation have started entering discussions, making inventory control, private labels and premium mix increasingly important differentiators into FY27, it added.

The broader takeaway into FY27 is that Indian fashion retail is no longer competing only on growth. Premium players are trying to convert premiumisation into structurally higher productivity and customer stickiness, while value retailers are attempting to scale aggressively without compromising affordability or margins. The next phase of the cycle is therefore likely to separate players based on sourcing control, inventory discipline and ability to sustain profitability amid rising inflation and competitive intensity.

Shoppers Stop

Shoppers Stop delivered one of the strongest operating updates in the sector, with a 4.7 per cent like-for-like (LFL) growth in FY26, the highest in a decade, while premium mix rose to 69%. The key shift was the sharp outperformance of non-apparel categories, with watches, fragrances and handbags materially outperforming apparel, while beauty distribution revenue grew 81 per cent YoY.

Management commentary increasingly positions the company as a premium lifestyle and beauty platform rather than a traditional department store retailer. However, despite improving throughput, the company acknowledged that EBITDA margin normalisation could still take another two years as investments toward premium store upgrades, loyalty and customer acquisition remain elevated.

Arvind Fashions

Arvind Fashions continued focusing on improving growth quality rather than broad based scale. The company’s management commentary suggested that online B2C and own retail are increasingly becoming structurally margin accretive, while tighter channel control is improving inventory productivity and full price sell through.

Premium brands continued outperforming the broader portfolio, with management highlighting that growth drivers have now “fallen in place” across key brands. Importantly, Arvind appears to be moving toward a more asset light and productivity focused model, where sharper assortment planning, faster inventory churn and higher direct channel contribution are supporting profitability even in a muted discretionary environment.

Aditya Birla Fashion & Retail

While Aditya Birla Fashion and Retail’s ethnic wear continued supporting margins and profitability improved across key formats, management remained cautious around persisting losses in newer businesses and weaker categories. In FY26, the company increasingly centered on portfolio rationalisation, tighter inventory cycles and margin repair rather than aggressive growth acceleration.

Unlike peers leaning into premium ecosystem building or rapid rollout, ABFRL appears focused on stabilising profitability and improving capital allocation discipline across its diversified portfolio.

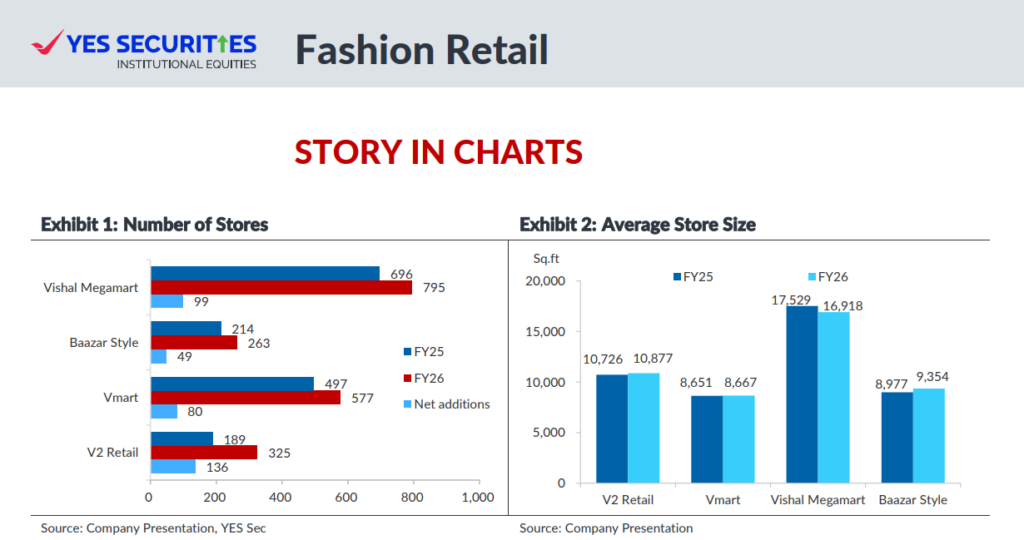

Vishal Mega Mart

Vishal Mega Mart continued to demonstrate that growth remains fundamentally footfall and customer acquisition-led, with management highlighting that most of SSSG came from higher customer visits rather than ticket expansion. The company added 105 stores during FY26, entered 77 new cities and continued scaling small format stores and quick commerce, signalling confidence that organised penetration in smaller towns remains underpenetrated.

With nearly 74 per cent contribution from private labels, management also indicated confidence in absorbing part of raw material inflation while maintaining sharper pricing gaps versus national brands.

V2 Retail

V2 Retail remained the sector’s most aggressive expansion story, adding 136 stores during FY26 while maintaining nearly 92 per cent full price sales contribution. Management commentary suggested that low absolute price points, sourcing efficiencies and improving merchandise mix should allow inflation pass through without materially impacting demand. Importantly, newer stores continue ramping up faster without visible dilution in store level productivity despite the pace of expansion.

V-Mart Retail

V-Mart Retail continued taking a more measured approach, prioritising throughput, profitability and return ratios over aggressive rollout. Commentary around Unlimited stores turned more constructive, with newer stores approaching or exceeding V-Mart productivity levels.

Unlike peers, V-Mart also explicitly flagged polyester yarn inflation and sourcing pressures as near-term risks, while reiterating that it would rely on sourcing efficiencies and calibrated pricing rather than aggressive price hikes to protect affordability and margins.

V-Mart Retail Ltd continued taking a more measured approach, prioritising throughput, profitability and return ratios over aggressive rollout.

Most Popular

22 hours ago

FSSAI issues notices to KFC, Nestle, Flipkart

The regulator said food businesses must adhere to prescribed food safety standards and ensure…

1 day ago

How AI Tokens Are Re-Engineering Wall Street Economics

Just as the emergence of cloud computing more than two decades ago shattered traditional…

3 days ago

Grasim to invest ₹3,000 crore to expand Lyocell capacity in Karnataka

The firm Group plans to increase its Cellulosic Staple Fibre capacity beyond 1 million…

23 hours ago

Fraudulent websites, emails target football fans as soccer fever grips the world

Cyber criminals are the global interest exploiting FIFA World Cup 2026 by deploying fraudulent…