Analysis

09 - 06 - 2026

Data consumption boom, tariff hikes to drive recovery in India telecom

A structural shift towards intense data consumption and upcoming tariff resets are set to trigger a powerful compounding phase for the sector: Elara Capital

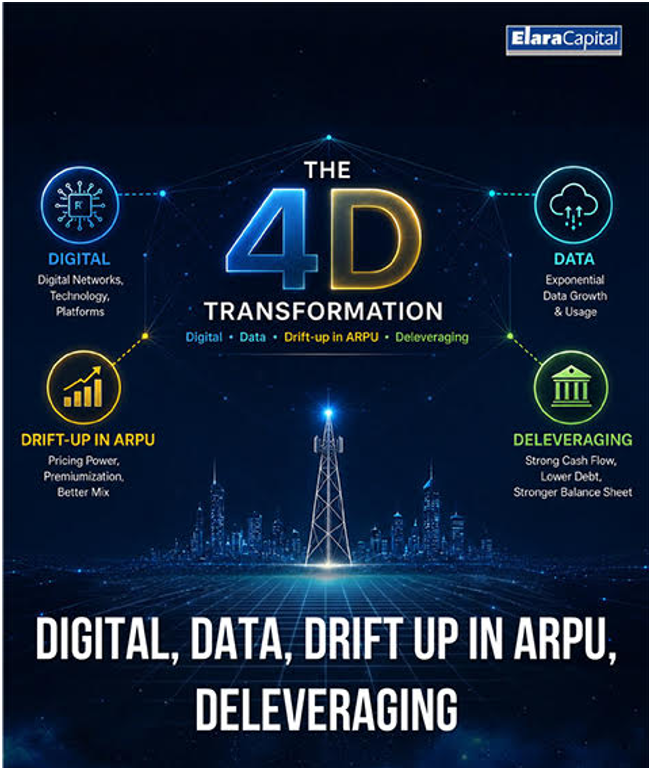

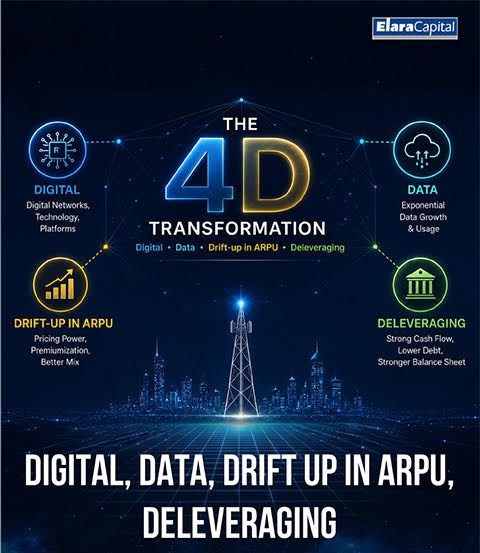

India’s telecom sector is entering a multi-year recovery driven by an average revenue per user (ARPU) compounded annual growth rate (CAGR) acceleration to 7 per cent in FY26-29.

The industry’s evolution from basic voice services to full-scale digitalisation is fuelling a data consumption boom in India and globally, setting the stage for a sustained rise in ARPU. Higher ARPU, improving cashflow generation and moderating capital expenditure (capex) would drive balance sheet deleveraging, Elara Capital said in a report.

“In our view, India’s telecom sector is in a multi-year recovery, driven by ARPU improvement, structural data demand, and lower incremental capex. This creates a favourable backdrop for earnings upgrade, deleveraging and higher free cashflow conversion,” Elara Capital said.

Key levers ahead include tariff trajectory, execution of bundling and enterprise monetization, capex pace involving fifth generation (5G) densification, and regulatory developments. As the sector transitions from consolidation to a compounding phase, free cashflow for operators is expected to grow in the double digits, it added.

India is at the forefront of this shift due to three structural changes: the most affordable tariffs, broad smartphone adoption, and extensive network expansion into the hinterlands. Industry consolidation from 17 operators to four, combined with sticky, high volume data use, is expected to reduce India’s tariff gap with global markets and restore attractive returns on invested capital.

Data usage surges

The next phase will be deeper and more durable, driven by higher engagement intensity, new data-heavy applications (video, Cloud gaming, enterprise SaaS and Internet of Things) and broader digital integration across consumer and enterprise use cases.

“We see a credible path for per-subscriber use to exceed 65GB per subscriber in the next decade from 21GB in CY24,” it said.

The ARPU growth trajectory is supported by tariff hikes, richer bundled service offerings, elevated data use being a staple behaviour, and disciplined pricing even if new market entrants arise. Blended ARPU is expected to rise to 6 per cent in FY27, 8 per cent in FY28, and 6 per cent in FY29, driven by tariff resets and higher average consumption.

With consolidation largely complete, India’s telecom industry is entering its strongest phase for cashflow generation and balance sheet repair. A quasi-duopoly market with some of the world’s lowest tariffs implies meaningful upside from tariff normalisation, which should translate into stronger free cashflow generation, lower leverage, and improving returns.

Among individual players, Reliance Jio, which is not listed, is transitioning from a scale-led telecom operator to a monetisation-driven digital platform. Backed by its integrated technology stack, Jio is building a scalable and structurally differentiated digital infrastructure ecosystem with strong long-term earnings visibility.

Valuation

Elara Capital believes Jio’s enterprise value is about ₹12-13 trillion based on 100,000 lakh crore (13x) FY28 EV/EBITDA. Jio Platforms’ EV could be about ₹13-14 trillion based on 13x FY28 EV/EBITDA, as considered in sum-of-the-parts (SOTP) value of Reliance Industries

The brokerage has initiated coverage on Bharti Airtel with a Buy rating for a target price of ₹2,387, Bharti Hexacom with a Buy rating and a TP of ₹1,756 and Indus Towers with an Accumulate rating and a TP of ₹491.

Most Popular

19 hours ago

Infosys Faces AI-Driven Price War, Loses Three Global Contracts

Infosys is confronting the new realities of the global outsourcing business after reportedly losing…

3 days ago

Indian’s Education Minister Dharmendra Pradhan resigns

In an X post, Pradhan said the resignation was to prevent anti-national forces from…

3 days ago

Pralhad Joshi given additional charge of Education Ministry

This follows the resignation of Dharmendra Pradhan amidst intense, weeks-long protests over alleged exam…

1 day ago

After Aadhaar, Nilekani to solve India’s exam trust crisis

The Indian government’s decision to appoint Nilekani to head a high-powered task force on…