Press Releases

11 - 05 - 2026

Press Release: With $1.7B in One Quarter, Delhi NCR Cements Place on India’s Tech Map

Gurugram led the regional funding landscape with 52% of total capital ($876M) in Q1 2026, followed by Noida at 27% ($453M) and Delhi at 20% ($341M) – with the three cities collectively accounting for 99% of all funding across the ecosystem. Faridabad ($431K) and Ghaziabad ($160K) remained marginal funding destinations.

KEY HIGHLIGHTS

- $1.7B raised across 110 rounds in Q1 2026. The top three deals accounted for $1.2B – leaving the remaining 107 rounds to split just $500M. Capital is not disappearing; it is being channelled into fewer, larger bets.

- Late Stage funding reached $1.2B in Q1 2026, down 21% from $1.5B in Q1 2025, yet the bulk of capital flowed into just two deals. Capital is consolidating into fewer, larger bets rather than spreading across the late-stage field.

- Enterprise Infrastructure led all sectors with $869.1M in Q1 2026, with the bulk of capital concentrated in a single data center deal. This signals that infrastructure is being treated as essential capital expenditure rather than speculative venture.

- Brahma’s $1.2B acquisition by Polymarket stood as the quarter’s largest single exit by a significant margin. This underscores that strategic acquisitions are delivering more immediate liquidity than public markets in the current environment.

- Gurugram led Delhi NCR’s funding landscape with 52% of regional capital ($876M) in Q1 2026, followed by Noida at 27% ($453M). Together, the two cities absorbed nearly 80% of all funding raised across the ecosystem in the quarter.

11th May 2026 – Tracxn Technologies Limited, a leading data intelligence platform, today released the Delhi NCR Tech Quarterly Funding Report – Q1 2026, covering equity funding activity across Delhi, Gurugram, Noida, Faridabad, Ghaziabad, etc. from 1 January to 31 March 2026.

Delhi NCR’s tech ecosystem raised $1.7B across 110 rounds in Q1 2026 – a market that, on the surface, appears softer than Q1 2025’s $1.9B but tells a more nuanced story beneath it. The drop in total funding masks a profound shift in capital structure: deal count fell to 110 from 153 in Q1 2025, yet three deals alone – Nxtra’s $710M PE round, Inox Clean Energy’s $344M Series D, and Wingify’s $150M Series A – accounted for $1.2B, or 71% of the quarter’s entire haul. This is not a market in retreat; it is a market in selection.

Capital Is Concentrating, Not Retreating

Delhi NCR Tech raised $1.7B across 110 rounds in Q1 2026, with deal volume falling 28% from 153 rounds in Q1 2025, while total funding declined only 11% – reflecting larger individual cheques rather than a broad pullback. Late Stage raised $1.2B, Early Stage $362M, and Seed Stage $147M. Three deals defined the quarter across stages – Nxtra ($710M, PE), Inox Clean Energy ($344M, Series D), and Wingify ($150M, Series A) – with the next-largest deal at $57M, underscoring how steeply capital was tiered across the ecosystem.

At the Seed Stage, Inflection Point Ventures led with 4 investments, followed by India Accelerator and Venture Catalysts with 3 each. Peak XV Partners, Saama, and Bain Capital Ventures were the most active at the Early Stage, while Orbimed, Blume Venture, and Swedfund anchored Late Stage activity – reflecting a mix of domestic and international institutional conviction across all funding levels.

Infrastructure and Clean Energy Rewrite the Sector Map

Enterprise Infrastructure commanded $869.1M in Q1 2026 – compared to just $624K in Q4 2025 – almost entirely driven by Nxtra’s data center round. Environment Tech took second place with $434M, anchored by Inox Clean Energy’s renewable energy raise. Enterprise Applications ranked third at $243M, supported by Wingify’s marketing optimisation platform funding. Together, these three sectors absorbed over $1.5B of the quarter’s $1.7B total, signalling a decisive shift in where large-scale capital conviction is being placed across the Delhi NCR ecosystem.

The top business models in Q1 2026 reinforce this structural rotation. Data Center Providers led with $710M from a single round, followed by Advanced Solar Energy Generation at $344M and Marketing Optimization at $150M. B2C Grocery Ecommerce, Electric Vehicles Manufacturers, and EV Charging Solutions also featured in the top ten, but with significantly smaller capital allocations – $40.4M, $49M, and $27.8M respectively. The message to founders and investors is clear: the region’s capital is aligning with infrastructure durability over consumer velocity.

Exits: Strategic Acquisitions Outshine a Quiet IPO Window

Delhi NCR recorded 9 acquisitions in Q1 2026 – matching Q1 2025’s count – while the IPO market delivered only a single listing. Novus Loyalty went public in March 2026 with a market cap of $24.1M, a fraction of the scale seen in prior periods. The contrast with the acquisition market is sharp: Brahma was acquired by Polymarket for $1.2B – the quarter’s standout exit by a significant margin. CarInfo’s acquisition by Cars24 for $44.4M was the next largest disclosed deal.

The remaining seven acquisitions in Q1 2026 – including Forest Essentials by Estée Lauder, Internshala by upGrad, and Solethreads by Tauseef Mirza – did not disclose acquisition prices, but collectively point to a maturing ecosystem where strategic buyers are actively consolidating complementary assets. High-profile international acquirers such as Polymarket and Estée Lauder entering the Delhi NCR exit roster signals that the region is producing companies compelling enough to attract global strategic interest – even when the public market window remains narrow.

Gurugram Leads, But the Whole Region Has a Story to Tell

Gurugram led the regional funding landscape with 52% of total capital ($876M) in Q1 2026, followed by Noida at 27% ($453M) and Delhi at 20% ($341M) – with the three cities collectively accounting for 99% of all funding across the ecosystem. Faridabad ($431K) and Ghaziabad ($160K) remained marginal funding destinations.

About Tracxn

Tracxn Technologies Ltd. is a data intelligence platform for private market research, tracking 7.5+ million entities through 2900+ feeds categorised across industries, sub-sectors, geographies, and networks globally. It has become one of the leading providers of private company data and ranks among the top five players globally in terms of the number of companies and web domains profiled.

Most Popular

24 hours ago

JioHotstar to hire for over 75 specialised roles in AI push

The Indian streaming platform is restructuring its media value chain by introducing non-traditional job…

3 days ago

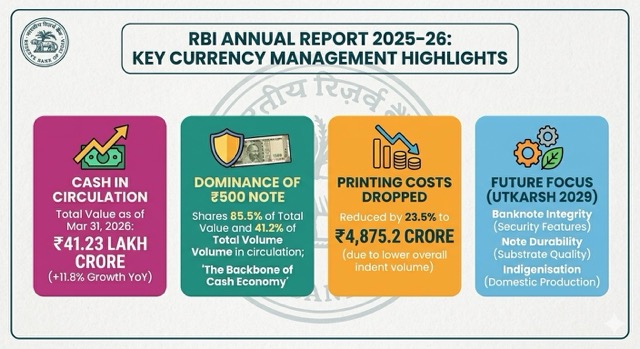

Cash is King, says RBI Annual Report for FY26

RBI's retail Central Bank Digital Currency (CBDC) pilot has encountered a speed bump

3 days ago

India’s BrahMos export push gains momentum

India’s BrahMos missile export drive is gathering pace, with Vietnam already having signed a…

4 days ago

US sanctions Indian firm as energy fight widens

India has no blocking statute that would shield local firms from foreign sanctions in…