News

13 - 05 - 2026

Press Release: PVs steering towards record sales of 5.9 million units this fiscal

GST tailwind holding but West Asia conflict, regulations will add to cost and investment pressures

May 13, 2026 | Mumbai

India’s passenger vehicle (PV) industry is set to see overall sales volume accelerate 5-7% to ~5.9 million units—its highest ever level—this fiscal, riding on the reduction in the goods and services tax (GST) last September and sustained consumer preference for utility vehicles.

But the operating environment is changing. While the GST tailwind continues, utility vehicles share has risen to 67% last fiscal and further gains are expected to be gradual. Rising input costs due to the West Asia conflict and expanding regulatory compliance requirements are factors to watch even as domestic demand stays healthy.

Our analysis of passenger vehicle makers accounting for about 94% of the wholesale volume indicates as much. For the record, domestic volume forms ~86% of the output and exports the rest.

The GST rate cut transformed demand for passenger vehicles last fiscal, propelling volume by 16.7% in the second half, reversing a 1.4% decline in the first half and lifting the full-year domestic growth to 7.9%.

Says Anuj Sethi, Senior Director, Crisil Ratings, “The GST tailwind will continue in fiscal 2027, though its intensity will moderate gradually. The small car segment, at ~30% of domestic volume, is expected to grow 2-4% on improved affordability and renewed first-time buyer interest amid a stable interest rate environment. Utility vehicles will continue to lead with 7-9% growth driven by a structural consumer preference for larger feature-rich vehicles and a widening model range across price points. We expect their share in the overall volume mix to continue rising from 67% last fiscal to 69% in fiscal 2027.”

The West Asia situation, however, bears watching on two counts. First, any meaningful rise in fuel prices could dampen demand as conventional fuel1 based vehicles still dominate the domestic market. Second, after a strong 17.5% uptick in fiscal 2026 to 0.9 million units, with West Asia accounting for about 25% of the total export volume, export growth is set to slow to 6-8% this fiscal, on account of the ongoing conflict impacting demand and a sharp rise in transportation costs.

Says Poonam Upadhyay, Director, Crisil Ratings, “The West Asia conflict has pushed up commodity prices and freight costs sharply. Most manufacturers have taken calibrated price hikes of 1-3% so far this fiscal, passing on only a part of cost increase to protect volume momentum. The GST cut of September 2025 had reduced prices by 11-13% on sub-4 metre vehicles, forming little over half of the total volumes. With prices in this segment still well below pre-reform levels, demand impact is expected to remain limited and volume momentum likely to hold, provided there is no significant rise in fuel prices.”

The industry is simultaneously entering a transformative regulatory phase. The Corporate Average Fuel Efficiency (CAFE)-III norms take effect from April 1, 2027 through fiscal 2032, Bharat Stage VII emission standards are also on the anvil, and the government is also considering higher ethanol blending targets. Together, these will progressively add to manufacturers costs and investment requirements.

Electric vehicles, at ~5% of the passenger vehicle volume, stand to benefit from this regulatory push over time. Charging infrastructure, however, remains the critical enabler and its pace of development will determine how quickly penetration can scale. The pace of cost pass-through to buyers will remain a key monitorable as the regulatory cycle unfolds.

Revenue is expected to grow 9-10% this fiscal, largely volume-led, with incremental support from calibrated price hikes. However, rising costs of steel, aluminium, copper and platinum group metals, compounded by elevated shipping costs, will compress operating margins by 50-80 basis points to 9.7-10% (~10.5% last fiscal). Despite this, near debt-free balancesheets and robust liquidity will keep credit profiles healthy even as these cost pressure persists.

The West Asia developments and their impact on commodity prices, fuel prices and supply chains, implementation of new regulations, and consumer response to further price increases will be the key factors to watch as fiscal 2027 unfolds.

Most Popular

2 hours ago

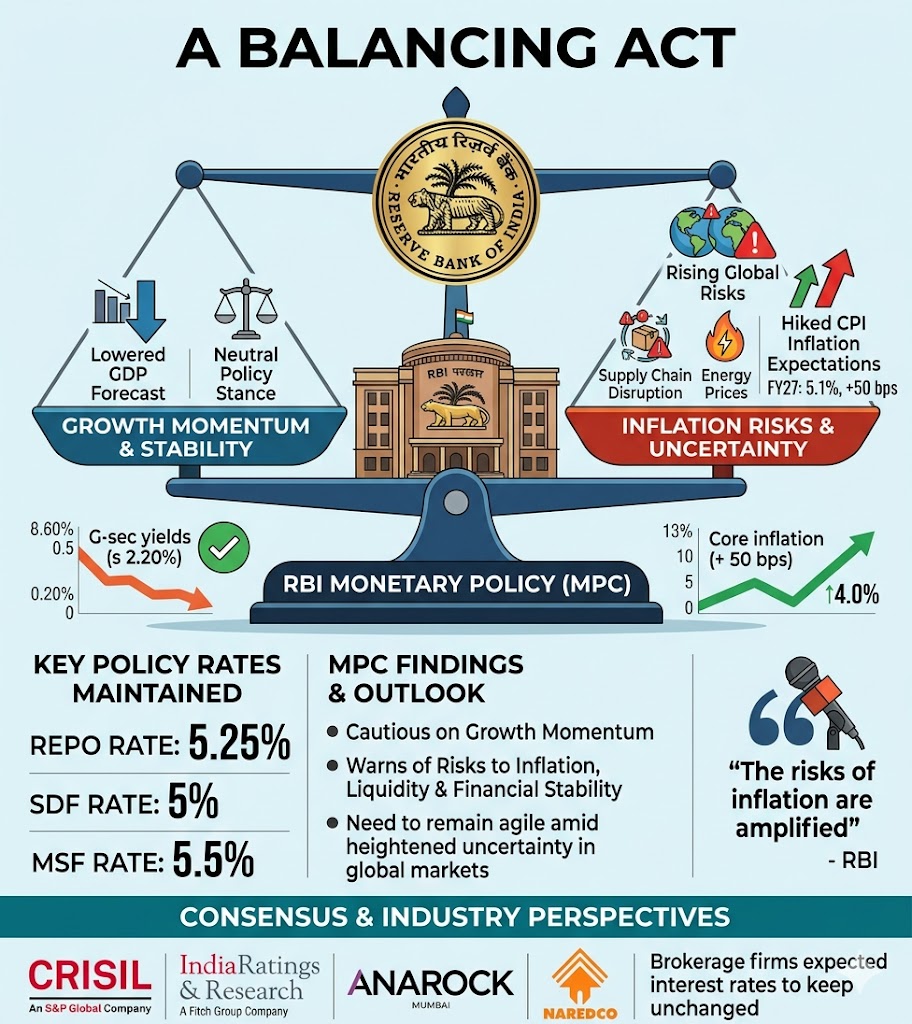

RBI keeps repo rate at 5.25% amid slowing growth, rising inflation risks

RBI has prioritised market agility and financial stability by freezing interest rates, even as intensifying geopolitical tensions force a sharp upward revision to inflation forecasts.

4 hours ago

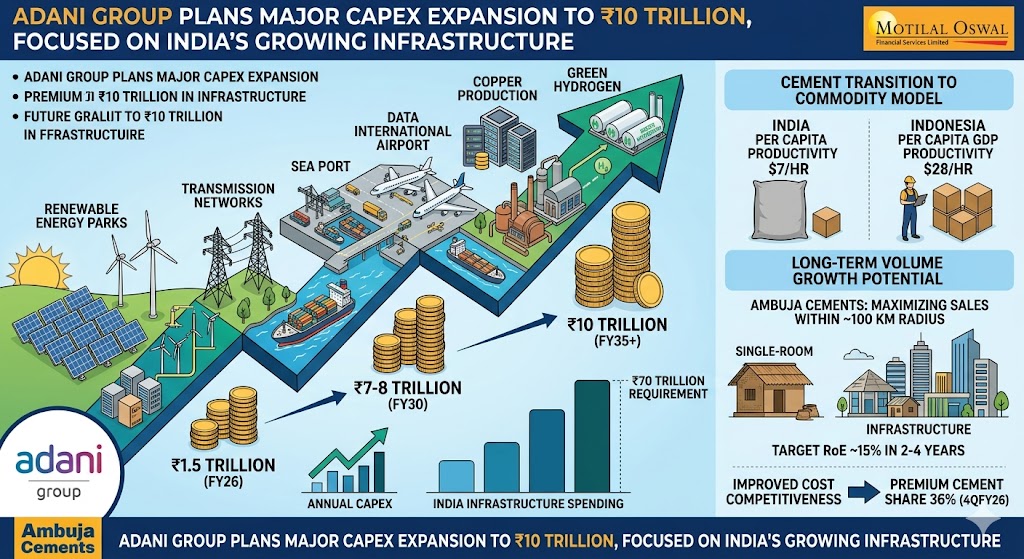

Adani Group to hike capex to ₹7-8 lakh crore by FY30

The group had invested ₹1.5 trillion in FY26, the largest by an Indian corporate.

4 hours ago

India polishes G-Sec investment rules for FPIs

The Central Government has eliminated Capital Gains Tax on foreign investments in government securities, enhancing the attractiveness of Indian sovereign bonds for international investors. This initiative coincides with India’s efforts to draw stable foreign capital amidst global uncertainties, rising oil prices, and intermittent pressures on the rupee. By enhancing post-tax returns for foreign investors, India …

4 hours ago

RBI eases path for global Indian capital to come home

This represents one of the most extensive capital-attraction initiatives in recent times To support India’s external financing position in the face of global uncertainty, the Reserve Bank of India (RBI) has undertaken one of the most extensive initiatives in recent years, relaxing foreign investment regulations concerning government bonds, equities, external commercial borrowings (ECBs), FCNR(B) deposits, …