News

13 - 05 - 2026

Industry seeks gold monetisation, urge exchanging old jewellery before price hikes

India holds an estimated 25,000 tonne of gold sitting idle in homes, and unlocking even a fraction of that would help in reducing the country’s dependence on imports

Our Bureau

Mumbai

India’s jewellery sector has called for a structured gold monetisation scheme and urged consumers to exchange old ornaments for new pieces, after the government raised import duty on gold and other precious metals in a move set to push up costs nationwide.

Calls for a structured gold monetisation scheme reflect a growing consensus that mobilising domestic holdings could ease pressure on imports and strengthen the trade.

“We believe this is the right moment for the industry and the government to come together and formalise a robust gold monetisation scheme. India holds an estimated 25,000 tonne of gold sitting idle in homes,” Raghav Dhir of Dhirsons Jewellers (Dhiraj Dhir Group) said.

Unlocking even a fraction of that through a credible, consumer-friendly programme would reduce India’s dependence on imports, ease forex pressure, and fuel domestic trade.

“The policy intent is clear; what we need now is a structured mechanism that gives consumers the confidence to participate,” he added.

Talking about the hike in import duties on precious metals, he added, it was a significant policy shift and will inevitably push up costs. However, this is also an “timely opportunity” for consumers to rethink how they engage with gold.

“We strongly encourage our customers to bring in their old gold and exchange it for new jewellery. This is one of the smartest ways to stay ahead of rising prices while refreshing your collection,” Dhir added.

India has sharply raised customs duties on imports of gold, silver and platinum in a bid to safeguard foreign exchange reserves, heightened by the global uncertainty stemming from the West Asia crisis. The Ministry of Finance announced late Tuesday that the effective import tax on gold and silver has been hiked to 15%, and that of platinum to 15.4%.

Industry backs government

The All-India Gem and Jewellery Domestic Council (GJC) also backed the government’s decision, describing the increase in customs duty as a temporary measure taken in the national interest.

“GJC and the entire gems and jewellery industry stand firmly with the nation and respect the Government’s policy decisions taken in the larger national interest. We believe the increase in customs duty is a temporary and calibrated measure in the present economic scenario,” GJC Chairman Rajesh Rokde said.

He urged the industry to remain calm, noting that India’s jewellery sector had consistently demonstrated resilience and adaptability during challenging times. Rokde pledged that GJC would continue to work closely with the government and stakeholders to ensure stability, consumer confidence and sustained growth.

Earlier on Tuesday, Jefferies said in a report that customs duty on gold, which was reduced to 6% from the earlier 15%, could be increased again.

“Gold and jewellery are deeply connected with India’s economy, traditions, and savings culture. At this juncture, it is important for the trade fraternity to avoid panic and continue business with confidence and responsibility,” Avinash Gupta, Vice Chairman of GJC, said.

Gupta added that GJC fully supported the nation’s broader economic priorities and remained committed to constructive engagement with policymakers to safeguard the interests of artisans, traders and consumers, while ensuring long-term growth and stability of the sector.

India is the world’s second-largest consumer of gold, with imports meeting most of its demand. Higher duties typically raise costs for jewellers and can dampen consumer sentiment, particularly during peak buying seasons such as weddings and festivals.

In an address earlier, PM Modi urged households to adopt austerity measures and avoid buying gold jewellery for one year.

Most Popular

2 hours ago

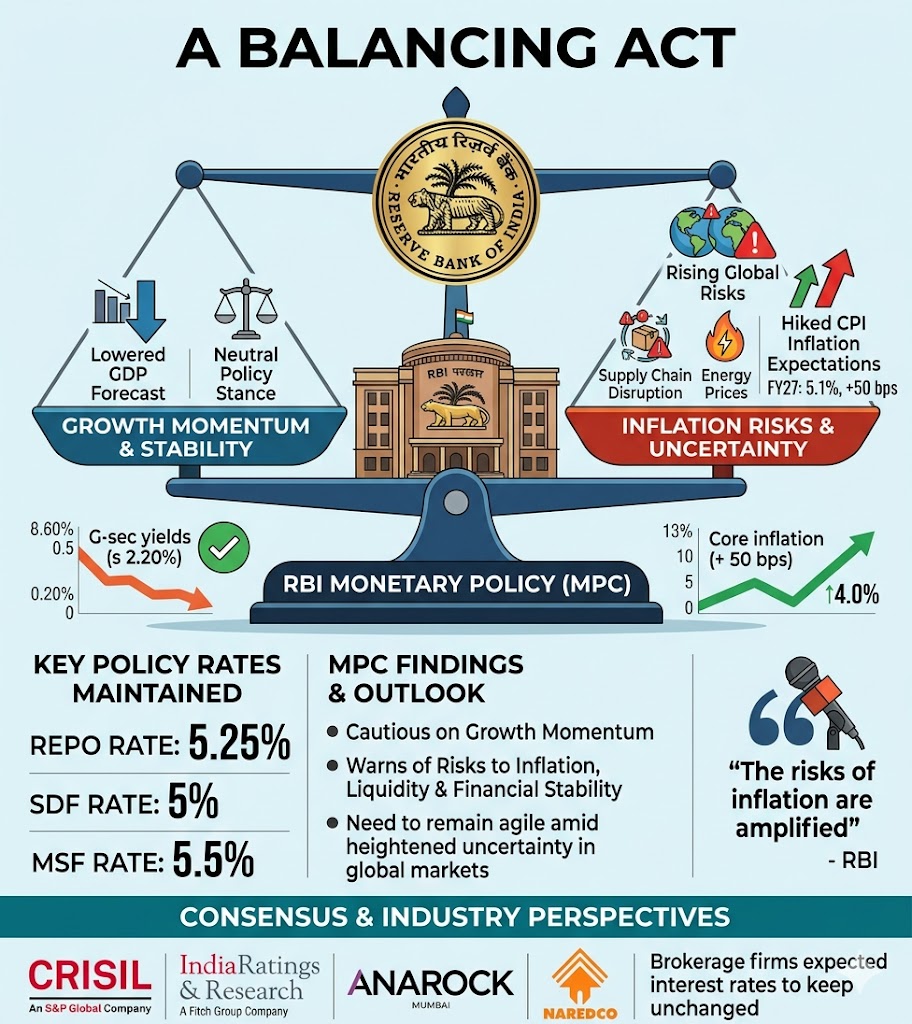

RBI keeps repo rate at 5.25% amid slowing growth, rising inflation risks

RBI has prioritised market agility and financial stability by freezing interest rates, even as intensifying geopolitical tensions force a sharp upward revision to inflation forecasts.

4 hours ago

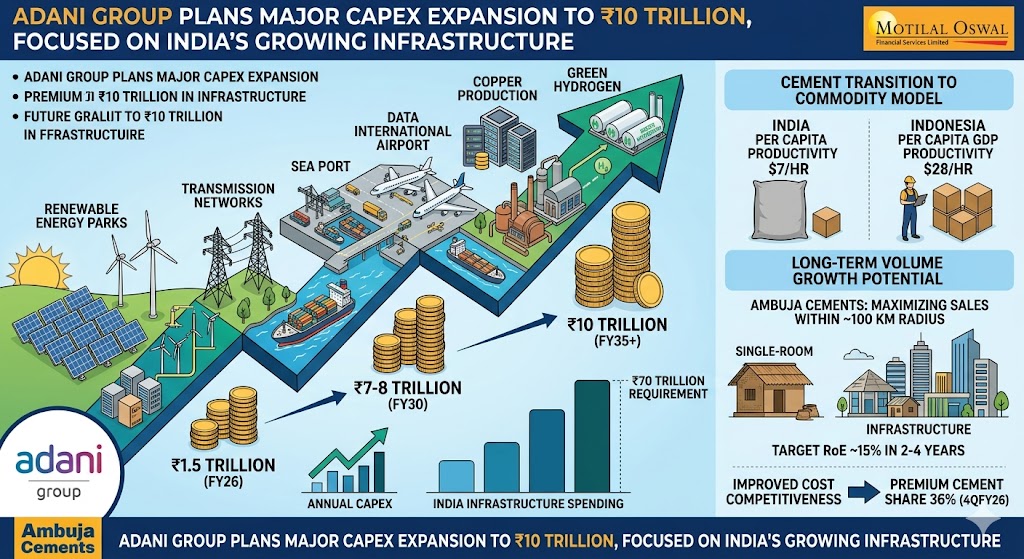

Adani Group to hike capex to ₹7-8 lakh crore by FY30

The group had invested ₹1.5 trillion in FY26, the largest by an Indian corporate.

4 hours ago

India polishes G-Sec investment rules for FPIs

The Central Government has eliminated Capital Gains Tax on foreign investments in government securities, enhancing the attractiveness of Indian sovereign bonds for international investors. This initiative coincides with India’s efforts to draw stable foreign capital amidst global uncertainties, rising oil prices, and intermittent pressures on the rupee. By enhancing post-tax returns for foreign investors, India …

4 hours ago

RBI eases path for global Indian capital to come home

This represents one of the most extensive capital-attraction initiatives in recent times To support India’s external financing position in the face of global uncertainty, the Reserve Bank of India (RBI) has undertaken one of the most extensive initiatives in recent years, relaxing foreign investment regulations concerning government bonds, equities, external commercial borrowings (ECBs), FCNR(B) deposits, …