News

05 - 05 - 2026

Ambuja Cements pares capex, shifts focus to profitability

The company’s capital expenditure for the financial year ending March 2027 has been cut to ₹6,000–6,500 crore, down from ₹7,500 crore in FY26.

By Our Bureau

Mumbai, May 5, 2026

Ambuja Cements Ltd, part of the Adani Group, is resetting its strategy to prioritise profitability and return on equity, with capital expenditure plans scaled back, brokerage Nuvama Institutional Equities said in a report on Tuesday.

The company’s capital expenditure for the financial year ending March 2027 has been cut to ₹6,000–6,500 crore, down from ₹7,500 crore in FY26. The firm had earlier targeted cement capacity of 117 million tonnes per annum (MTPA) by FY26 and 155 MTPA by FY28, with annual spending of about ₹8,000 crore. Management now expects capacity to reach 119 MTPA by FY27, compared with 109 MTPA at end-FY26, Nuvama said following an earnings call.

Some efficiency-related projects have been delayed by three to six months. Ambuja believes that without stronger profitability, fresh capital expenditure would dilute returns, and is instead focusing on improving margins through better distribution networks and lower raw material and energy costs.

Sales volumes rose 9% year-on-year to 19.9 million tonnes, but profitability per unit weakened. Earnings before interest, tax, depreciation and amortisation (EBITDA) per tonne fell 28% to ₹736, hit by a 7% rise in operating costs. The company’s long-term capacity goal of 140 MTPA has been pushed back by one to two years, with a new target of FY30, it said, adding, the management is concentrating on stabilising recently acquired assets, including Sanghi and Penna, rather than pursuing further large-scale acquisitions, Nuvama added.

Ambuja Cements Ltd has set capital expenditure for FY27 at ₹6,000–6,500 crore, with most of the allocation directed towards ongoing projects such as capacity expansion, waste heat recovery systems, fly ash handling, debottlenecking and routine maintenance, according to brokerage Motilal Oswal.

The firm reported consolidated revenue of ₹10,920 crore in the year to March, up 9% from a year earlier, but earnings before interest, tax, depreciation and amortisation (EBITDA) fell 22% to ₹1,460 crore. Analysts attributed the shortfall to higher operating costs.

The firm’s management has adopted a cautious stance on the sector, projecting industry demand growth to ease to about 5% in FY27. Despite this, Ambuja is targeting an 8% rise in consolidated volumes, aiming to outpace the broader market.

According to HDFC Securities Institutional Equities (HSIE), the company has guided for an 8% annual growth in volumes, with lower capex for FY27. Ambuja’s management has chosen to slow expansion and concentrate on operating expenditure reduction, aiming for savings of ₹500 per tonne between FY26 and FY28, following a weak cost performance in the second half of FY26.

In the March quarter of FY26, total volumes rose 8% while like-for-like volumes slipped 1%. Unit EBITDA was steady at ₹728 per tonne, reflecting limited pricing gains and higher operating costs. HSIEhas retained its “buy” rating with a target price of ₹580 per share, valuing the company at 15.5 times its consolidated FY28 estimated EBITDA.

In its report, brokerage Systematix Institutional Equities said that the reduction in capex reflects a more disciplined approach to capital allocation and optimisation of existing assets. Of the total capex of ₹6,000–6,500 crore, about ₹400 crore is earmarked for ongoing projects and the balance directed towards debottlenecking and maintenance. The company is targeting an internal rate of return of 18% on these projects.

For Ambuja Cements, organic growth remains the priority, with new clinker lines planned at Mundra and Assam, each of 2 million tonnes per annum, alongside grinding units closer to demand centres such as Bihar. Ambuja expects to reach 119 MTPA by end-FY27, supported by 10 million tonnes of new grinding capacity, Systematix said.

On costs, the management in the earnings call highlighted delays in fly ash infrastructure, which have kept raw material expenses elevated. Savings of ₹150–200 per tonne are anticipated once systems are operational, aided by green energy initiatives. Freight costs rose in the March quarter due to longer transport leads and higher packing expenses, partly linked to disruptions from the West Asia conflict.

The ramp-up of Sanghi’s utilisation is tied to marine infrastructure, with seven vessels ordered for phased delivery from next year. During FY26, Ambuja expanded total cement capacity to 109 MTPA, driven by 10.7 MTPA of new grinding units and 7 MTPA of clinker additions at Jodhpur and Bhatapara. Further additions are planned in H1FY27, including a clinker unit at Maratha, taking capacity to about 119 MTPA.

Ambuja Cements reported a subdued March quarter, with revenue broadly in line but earnings before interest, tax, depreciation and amortisation (EBITDA) falling short of expectations due to lower volumes, weaker realisations and persistent cost inflation, brokerage Centrum Institutional Research said.

Centrum highlighted multiple cost headwinds, including higher kiln fuel expenses, clinker inventory build-up, longer transport leads during plant shutdowns, and elevated branding, packaging and tax costs. Additional pressures stemmed from supply constraints in packaging and labour migration during state elections.

Centrum said Ambuja’s strategic shift towards ramping up utilisation before fresh capacity additions underscores disciplined capital allocation and a focus on maximising return on capital employed. Over the medium term, benefits from ongoing expansions, better use of acquired assets, merger synergies, premiumisation and cost optimisation are expected to support earnings.

Most Popular

2 hours ago

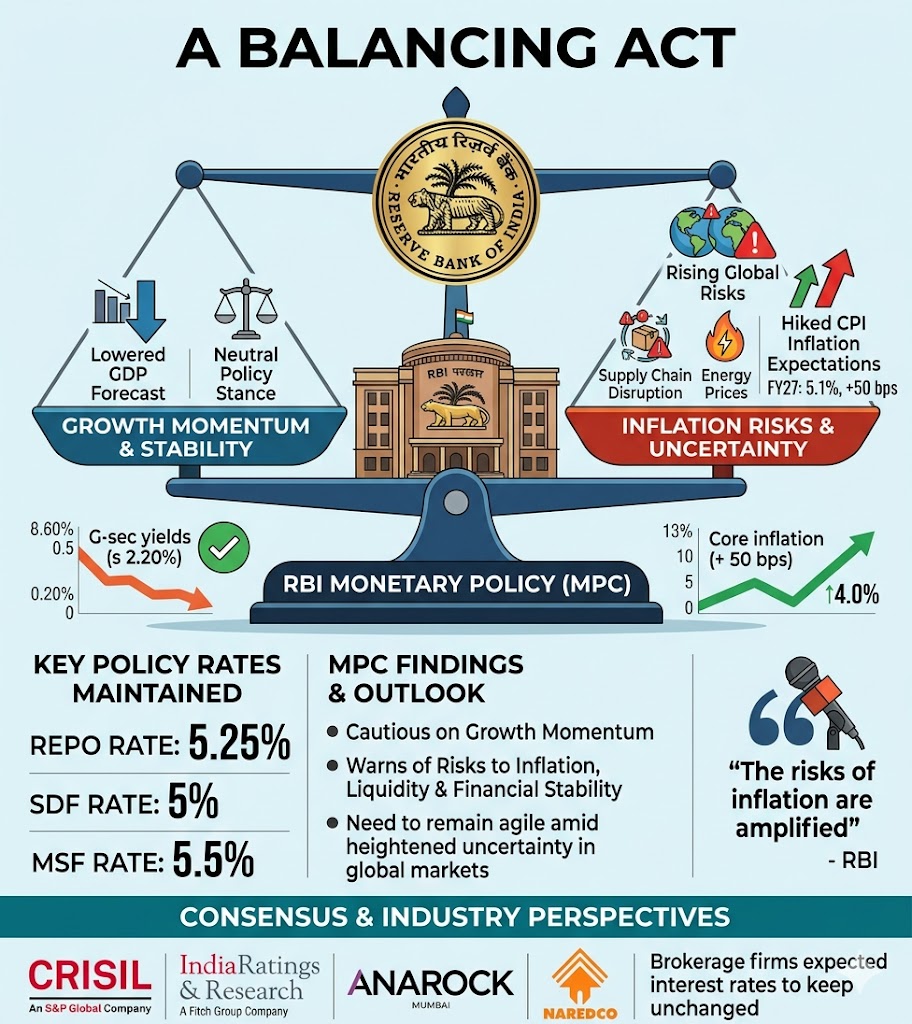

RBI keeps repo rate at 5.25% amid slowing growth, rising inflation risks

RBI has prioritised market agility and financial stability by freezing interest rates, even as intensifying geopolitical tensions force a sharp upward revision to inflation forecasts.

4 hours ago

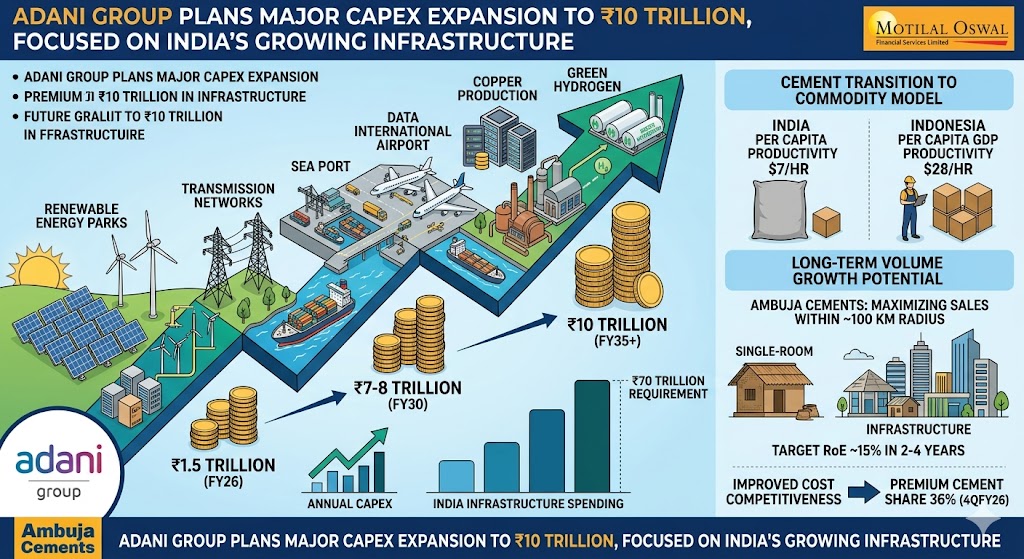

Adani Group to hike capex to ₹7-8 lakh crore by FY30

The group had invested ₹1.5 trillion in FY26, the largest by an Indian corporate.

4 hours ago

India polishes G-Sec investment rules for FPIs

The Central Government has eliminated Capital Gains Tax on foreign investments in government securities, enhancing the attractiveness of Indian sovereign bonds for international investors. This initiative coincides with India’s efforts to draw stable foreign capital amidst global uncertainties, rising oil prices, and intermittent pressures on the rupee. By enhancing post-tax returns for foreign investors, India …

4 hours ago

RBI eases path for global Indian capital to come home

This represents one of the most extensive capital-attraction initiatives in recent times To support India’s external financing position in the face of global uncertainty, the Reserve Bank of India (RBI) has undertaken one of the most extensive initiatives in recent years, relaxing foreign investment regulations concerning government bonds, equities, external commercial borrowings (ECBs), FCNR(B) deposits, …